Key information

Main city: Dakar, Senegal.

Scope: National level

Lead organisations: Senegalese Tax Administration (DGID)

Timeframe: 2019 – ongoing

Themes: Land and connectivity; Economy and finance; Infrastructure; Land; Metropolitan management; Public administration and governance

Main funder agencies: Senegalese Tax Administration (funding); International Centre for Tax and Development (ICTD) under the FCDO’s Economic Development and Institutions programme (technical assistance and funding); French Development Agency (funding and technical support); African Development Bank (funding); World Bank (funding).

Approaches used in initiative design and implementation:

- Digitalised data collection methods.

- Improving information-sharing systems.

- Property identification and registration.

- Simplified valuation methods.

- Targeted communication.

Initiative description

Background and context

Property taxes remain one of the most underused sources of local revenue in sub-Saharan Africa, even as cities face increasing demands to deliver basic services and manage rapid urban growth. While they hold considerable potential, actual collections tend to be very low – usually less than 0.5% of GDP, compared to between 1% and 2.5% in OECD countries. In Senegal, the figure is even lower, with property tax revenues contributing just 0.3% of GDP – roughly a fifth of what could be raised.

Dakar Region is a clear example of the wider challenges facing property tax systems in the region. Despite being a densely built and fast-growing metropolitan area with considerable potential to raise local revenue, property tax collections remain low. Only about 61,000 properties were listed on the tax roll before the reform, compared to an estimated total of 370,000 – representing a registration rate of roughly 16%. Payment rates are also weak: in 2022, only 10% of issued tax bills were paid, and actual collections amounted to just 16% of total assessed liabilities (Knebelmann et al., 2024).

Several factors account for these gaps. Compliance remains weak, as the system continues to rely heavily on self-declaration, with few incentives for taxpayers to comply and little motivation for the centrally managed revenue administration to enforce collection, since property tax revenues primarily accrue to local governments (Nyirakamana et al., 2024). Property records are outdated, both in terms of addresses and taxable values, partly due to the cadastre-first approach, which requires properties to be legally registered with complete information – such as lot numbers and ownership details – before they can be taxed (Prichard et al., 2025). This is compounded by the absence of a consistent addressing system and unique property or taxpayer identifiers, as well as valuation methods that remain complex and inconsistently applied, resulting in an incomplete and obsolete valuation roll (Knebelmann, 2019). Coordination across institutions is also fragmented. The Directorate General of Taxes and Domains (DGID) is responsible for identifying and valuing properties and issuing tax notices, while the General Directorate of Public Accounting and the Treasury (DGCPT) handles billing, collection and enforcement. Revenues are transferred to municipal accounts and, under the General Local Government Code, are intended for essential local services. However, limited collaboration between the DGID, municipalities and the Treasury, alongside the use of separate and non-interoperable databases by the DGID and Treasury, continues to undermine coordination and constrain the overall performance of the property tax system (Knebelmann, 2019; Nyirakamana et al., 2024; Mukazayire et al., 2025b).

Summary of initiative

Since 2017, efforts to modernise Senegal’s property tax system – led by the DGID, a central agency under the Ministry of Finance – have focused on improving property registration and expanding the tax base by digitising key stages of the fiscal chain (Knebelmann, 2019; Prichard et al., 2025). Anchored in a cadastre-first approach to property taxation, which requires land to be legally registered and assigned parcel numbers linked to property owners before it becomes taxable (Prichard et al., 2025), the reform has followed a phased strategy to progressively update and extend the national cadastre. Initially rolled out and tested in the Dakar Region (Knebelmann et al., 2021a) the initiative now forms part of a wider national programme (Nyirakamana et al., 2024).

Between 2019 and 2023, three major programmes were launched to support these efforts. The Programme d’Amélioration de la Gestion des Contributions Foncières (Programme for the Improvement of Property Tax Management, PAGCF) conducted censuses in 26 municipalities in Dakar. The Programme d’Appui aux Communes et Agglomérations du Sénégal (Support Programme for Senegal's Communes and Agglomerations, PACASEN) extended this to 124 high-potential municipalities, including Dakar and regional capitals. And the ongoing Recensement National des Propriétés Immobilières (National Real Estate Property Census, RNPI), part of the Plan Yataal, aims to expand the property tax base nationwide, covering all departments not included in previous initiatives (Nyirakamana et al., 2024).

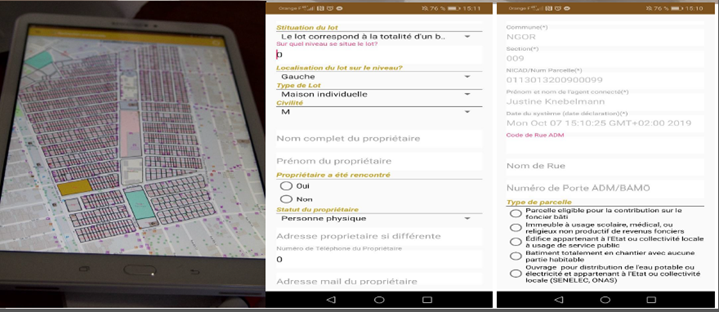

At the heart of these innovations is an investment in information technology designed to update the legal cadastre by collecting detailed property information and using this data to revise the fiscal cadastre through the identification of taxable properties and the estimation of the tax base (Nyirakamana et al., 2024). To this end, a new property tax management software has been introduced to support field data collection, automate tax calculations and generate tax notifications. The system features an Android-based tablet application integrating GPS and GIS technologies, which enables field agents to record key property details, such as location, cadastral ID, physical characteristics, estimated rental value, owner information and photographs. It automatically computes tax liabilities, updates the taxpayer database and produces geocoded tax notices, streamlining what was once a fragmented manual process (Knebelmann et al., 2021a).

A simplified valuation method has also been piloted and integrated into the property tax management software. Using a points-based formula, a streamlined version of a computer-assisted mass appraisal (CAMA) system, it relies on observable features, supported by satellite and drone imagery, to generate rental value estimates directly within the application, reducing reliance on spontaneous declarations or assessor discretion (Knebelmann and Pouliquen, 2021). These digital innovations, first tested in the Dakar Region, are supported by interoperable computer systems that strengthen interdepartmental coordination, facilitate monitoring of census activities, share information between the tax administration and the Treasury, and improve the processing of tax data (Nyirakamana et al., 2024).

Technical reforms have been complemented by public awareness and communication campaigns designed to inform citizens about property censuses and encourage participation. Using mass media, social platforms and in-person community engagement, the campaign has helped explain the reform process and its benefits (Mukazayire et al., 2025a). Messaging is delivered in both Wolof and French to ensure accessibility, while training for neighbourhood delegates fosters local ownership and encourages participation on the ground (Mukazayire et al, 2025a).

A phased intervention

Dakar’s property tax intervention followed a phased trajectory, beginning in 2017 with a diagnostic and design phase conducted with international researchers, which led to the development of a new property tax management system to address weaknesses in the existing framework and establish a sustainable, nationwide taxpayer registration process. The digitalisation initiative focuses on automating the fiscal chain to enhance data management, coordination and transparency. Over two years, the project team collaborated with the administration and a local IT firm to develop an Android and web-based application to streamline these processes.

In 2019, the system was piloted through a randomised controlled trial involving a large-scale census in 97 cadastral sections across the Dakar Region, with 97 comparable sections serving as control areas to assess impacts on tax assessment, payment and compliance (Knebelmann, 2019). In 2020, system refinements were undertaken and census work continued, although progress was temporarily slowed by the Covid-19 pandemic. The intervention regained momentum in May 2021, when the census resumed using the digital application, now integrated into the DGID’s internal systems (Knebelmann et al., 2021a). By July, the programme had entered its scaling phase.

With evidence that the technology effectively identified and registered property owners, the DGID expanded the approach nationwide through two additional projects – PACASEN and RNPI/RNBI. Property registration increased substantially: by the end of 2023, over 160,000 properties had been recorded, a threefold rise from the previous database of about 50,000 taxpayers, though the pace of registration – at around 40,000 properties per year – remains slow relative to the scale of the task (Prichard et al., 2025). In 2021, the government also launched Yaatal, a mass communication campaign to inform citizens about the census and encourage participation (Mukazayire et al., 2025a).

Agencies and financing

The PAGCF, which included the development of the property tax management software, was implemented by the DGID in collaboration with the Paris School of Economics and supported by multiple donors, including the Economic Development Institution, ICTD, IGC, the Abdul Latif Jameel Poverty Action Lab Digital Identification and Finance Initiative and the Fund for Innovation in Development (Knebelmann et al., 2021a; Prichard et al., 2025).

A dedicated pilot on semi-automated valuation, “Developing points-based valuation”, was launched in late 2018 with ICTD funding. The project supported the calibration of a valuation model using local data from Senegal and Sierra Leone (Knebelmann and Pouliquen, 2021).

The PACASEN was jointly financed by the World Bank, French Development Agency and Government of Senegal, and coordinated by the DGID’s Bureau for Local Authorities (BCT) in collaboration with local governments through Local Tax Commissions (CFL) (World Bank, 2024; Prichard et al., 2025).

The RNPI is supported by the national government and the African Development Bank (Prichard et al., 2025).

Target population, communities, constituents or "beneficiaries"

The census programmes initially aimed to identify up to one million properties nationwide, both formally registered and informally held (Nyirakamana et al., 2024), including an estimated 374,000 plots across the entire Dakar Region (Knebelmann et al., 2021b). By June 2024, after nearly four years of implementation, over 200,000 properties had been registered – a fourfold increase from the DGID’s original database of about 50,000 property taxpayers nationwide. However, the registration rate of roughly 45,000 properties per year remains modest compared to cases such as Freetown, where more than 100,000 properties were recorded within just six months.

The broader expectation is that these property identification and registration reforms, designed to boost local government property tax revenues and unlock land-based wealth, will ultimately improve the delivery of public services and infrastructure (Barras et al., 2024) as an expanded property tax base is expected to enhance the fiscal capacity of communes (local governments) with revenues deposited into local accounts and, under the Code Général des Collectivités Locales, allocated to essential services and infrastructure.

ACRC themes

The following ACRC domains are relevant (links to ACRC domain pages):

- Land and connectivity (primary domain)

- Health, wellbeing and nutrition

- Informal settlements

- Neighbourhood and district economic development

While there is debate over whether property tax functions as a mechanism for unlocking land wealth potential, ACRC frames it as an instrument for redistributing land value without stimulating speculative increases. The property tax reform in Dakar can thus be situated within ACRC’s land and connectivity domain as an initiative to channel urban land value into public revenue amid complex institutional and territorial dynamics.

The reform aims to modernise fiscal and legal cadastres by leveraging information technology for property censuses, facilitating the collection of extensive property data and more efficient enumeration. Enhanced coordination across departments, supported by interoperable digital systems, has improved the monitoring of census activities and tax data processing, although persistent weak central–local collaboration and inter-agency fragmentation continue to hinder effective revenue mobilisation (Nyirakamana et al., 2024). The introduction of a simplified, semi-automated, points-based valuation system marks a departure from earlier opaque assessment practices. However, implementation remains constrained by a colonial-era legal framework requiring comprehensive property registration before taxation – a “cadastre-first” approach that slows the expansion of the tax base (Prichard et al., 2025). Nonetheless, the reform demonstrates important innovation while highlighting how land, territorial and institutional politics continue to shape reform paths.

The reform intersects with other ACRC domains: health, wellbeing and nutrition; neighbourhood and district economic development; and informal settlements, by expanding fiscal space for services and infrastructure, while drawing attention to the tensions between formal governance and informal land arrangements.

The following ACRC crosscutting themes are also relevant (links to ACRC domain pages):

Finance

The intervention is directly linked to ACRC’s finance crosscutting theme, as it forms part of the Plan Sénégal Émergent, which aims to elevate the country to emerging economy status by 2035. The plan prioritises the mobilisation of property taxes as a key mechanism for funding and financing urban infrastructure and services.

What has been learnt?

Effectiveness/success

How does the initiative define success?

The reform’s effectiveness centred on two core components. The first involves updating the legal cadastre through the systematic collection of detailed information on properties and their owners, while the second focuses on updating the fiscal cadastre by identifying taxable properties and estimating the tax base (Nyirakamana et al., 2024). In practice, these reforms resulted in operational improvements, including the streamlining of the fiscal chain, particularly through the experimental roll-out of a new property tax management system. Key innovations included the introduction of a digital application enabling large-scale property tax census operations; the adoption of a simplified, semi-automated valuation method (Knebelmann et al., 2021a; Choho, 2025); and the implementation of an improved information system integrating the various departmental platforms involved in property tax administration (Nyirakamana et al., 2024).

Overlap with the ACRC’s conceptual framework and theory of change

ACRC outlines four preconditions for urban reform, two of which are particularly salient in Dakar’s property tax reform: the formation of reform coalitions; and the development of state capacity. The reform has been implemented through a coalition comprising national actors (most notably the tax administration, DGID), international researchers and international funders, including the Economic Development and Institutions (EDI) programme, French Development Agency (AFD), African Development Bank, ICTD and World Bank. This coalition has effectively mobilised complementary technical and institutional expertise to advance reform.

As ACRC’s theory of change highlights, limited fiscal devolution has historically constrained local ownership and weakened citizen support for reform. Relations between municipalities and central agencies have gradually improved but were long characterised by weak administrative capacity and limited fiscal autonomy. Although municipalities are the main beneficiaries of property tax revenues, they historically played a marginal role in tax administration and census activities, while revenue mobilisation remained low due to the DGID’s limited incentives to prioritise local collection. Recent efforts such as new communication channels and incentive mechanismsʼ have strengthened collaboration, yet lingering tensions between municipalities and DGID’s deconcentrated offices, divergent motivations and mistrust at the Treasury level risk undermining progress and frustrating efforts to enhance property tax mobilisation (Nyirakamana et al., 2024).

The second precondition, building state capacity, understood as the recognition that sustainable urban reforms in African cities require not only technical solutions but also strong and capable public institutions, is also evident in Dakar’s approach. Although the reform has delayed immediate revenue gains – as the need to update the legal cadastre by collecting information, not only on properties but also on their owners, has slowed census activities (Nyirakamana et al., 2024) – it nonetheless represents a clear effort to modernise the cadastre through investment in information technology and enhanced coordination across departments and levels of government.

How successful has the initiative been?

At the national level, the census programmes registered over 200,000 properties out of a target of one million – four times the 50,000 recorded in the original DGID database, with an average rate of 45,000 per year. This pace, however, remains slow compared to other reform approaches, such as the property-tax-first model in Freetown, where more than 100,000 properties were registered in just six months (Prichard et al., 2025; Nyirakamana et al., 2024).

An assessment of the digital tools pilot initiative in the Dakar Region, based on a randomised control trial conducted between 2019 and 2023, demonstrates measurable success across the reforms’ key objectives. In property registration and valuation, the share of registered properties in 97 targeted cadastral sections rose from about 19% to 92%. Of these, 73% received printed tax notices, resulting in 26,412 new tax bills. The fiscal census also added roughly 100,000 properties citywide, significantly expanding the tax base (Choho, 2025). Administrative data show more complete and up-to-date property records, improved address accuracy, revised cadastral maps and digital links through QR codes. In tax compliance and revenue, the distribution rate of tax bills increased from 10% in 2021 to 56% by 2023, with 16,692 bills delivered, while the payment rate rose from 8.8% to 21.1%, corresponding to 4,435 bills paid. These gains generated an estimated USD 1.5 million in additional revenue for the National Treasury (DGCPT) (Choho, 2025).

Key lessons learnt

Software development and testing:

- Process design requires time: digitalising the property taxation process demands extensive cross-department coordination; this should precede software contracting.

- Inclusive and iterative testing: involving practitioners from all relevant departments in software testing at each stage improves adoption and usability.

- Securing access to code: partnering with a local IT firm supports long-term collaboration, bringing contextual knowledge and motivation; but securing access to the source code from the outset is essential to avoid vendor lock-in and ensure administrative autonomy (Knebelmann et al., 2021a).

Cadastre-first approach

- Cadastre-first limitations: requiring updating the legal land register and detailed documents on properties and their owners before taxation creates barriers due to high costs, complexity and institutional fragmentation.

- Alternative models: mixed or property-tax-first approaches, which focus on simpler identification processes and prioritise establishing an operational fiscal cadastre, can deliver faster and more feasible improvements (Nyirakamana et al., 2024).

Information sharing

- Interoperable systems are critical: fit-for-purpose IT tools must enable data sharing across agencies to avoid inefficiencies and revenue loss.

- Institutional coordination is key: without cross-agency cooperation, parallel systems and a lack of integration undermine the benefits of digital tax reform (Barras et al., 2024).

Understanding limitations

The cadastre-first approach has proven slower and more complex than anticipated. While conceptually sound, it relies on detailed registration of plots and owners, requiring high-quality data, significant funding and coordination across multiple agencies. Its rigid sequence – census, valuation, then enforcement – has delayed implementation and limited short-term revenue gains. Moreover, the requirement that properties be formally registered before being taxed has created insurmountable barriers to effective administration.

Digitalisation, though essential, demanded greater upfront investment in infrastructure and staff training than initially planned. Institutional fragmentation – particularly among the DGID, cadastre office and Treasury – has further hindered progress, due to weak coordination and limited data-sharing caused by incompatible systems. In response, efforts are underway to develop a shared IT platform to support regular database updates, reduce undelivered notices and enhance coordination.

Finally, the centralised nature of the reform has limited local authorities’ role in tax mobilisation, reducing responsiveness and accountability (Barras et al., 2024; Nyirakamana et al., 2024).

Potential for scaling and replicating

Senegal’s cadastre-first strategy holds potential for long-term institutional development, particularly in establishing a comprehensive and formalised property register. However, research suggests that in low-capacity contexts, beginning with a property tax-first approach – such as that adopted in Freetown – prior to full cadastral development may offer a more effective entry point (Prichard et al., 2025; Nyirakamana et al., 2024). By generating early revenue gains, this approach can help finance and support the gradual expansion of cadastral systems. In this light, a hybrid strategy that combines immediate tax mobilisation with phased land registration may provide a more balanced path, delivering early results while laying the foundation for more sustainable and institutionally robust reform over time.

Participating agencies

Further information

References

Choho, B (2025). “Potential for property taxation in Dakar, Senegal”. Presentation at ACRC Urban Property Tax Workshop, Accra, Ghana, 19-21 May 2025.

Cite this case study as:

Garcia, E (2025). “Property tax reform in Dakar, Senegal”. ACRC Urban Reform Database case study. Manchester: African Cities Research Consortium, The University of Manchester.